The real story behind PI premium hikes for financial advisers

Published

Read time

This article was originally posted on FTAdviser.com and can be found here.

The financial press has been full of tales of woe for financial advisers: increasing Financial Conduct Authority fees, increasing Financial Services Compensation Scheme levies, reducing income and ‘massively’ increased professional indemnity insurance costs.

As insurance brokers we speak to financial advisory businesses multiple times a day and try to assist in helping them navigate through these difficult times. We are not always able to help but, putting this aside, some of the stories do appear rather sensationalist.

As a result, I would like to provide some commentary on the PI insurance market to distinguish the facts from the fiction. I will also shed some light on what you can do to help your next insurance application.

Key Points

- There has been a lot of concern about rising PI insurance costs

- There is lack of supply in the insurance market

- Advisers can take steps to make their application easier

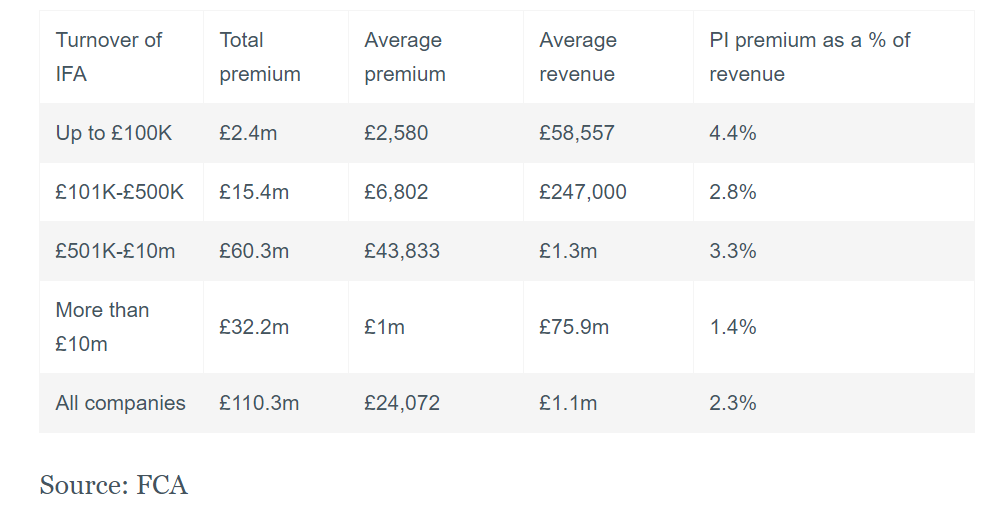

Any company that has had a recent renewal will know that premiums have increased; in fact they have done so consistently for two years, but a look at the table above (compiled from the FCA’s own figures) will put the premium rates (being premium as a percentage of turnover) into context.

These are the figures to the end of 2019 and there has continued to be premium price pressure through 2020 to date. Now, there is evidence that premium rises are slowing.

Of course, showing average figures does hide some of the variations. For example, a company that has undertaken a significant number of defined benefit pension transfers will likely pay a very different premium to one that principally advises on investment and protection policies.

Similarly, a company that has had a number of claims in the past compared with one that is claim-free will also pay a higher premium.

So what is driving these premiums?

- Lack of insurance capacity: with only five or six insurance markets and a general lack of interest in new business from these carriers, the ability to source competitive alternative quotes is extremely limited;

- Insurers’ concerns over the now maximum Financial Ombudsman Service award of £355,000 for complaints referred to Fos on or after April 1 2020 for acts or omissions by companies on or after April 1 2019. Complaints about acts or omissions by companies before April 1 2019 and which are referred to FOS after that date will remain at the maximum £160,000;

- The FCA’s continuing investigation of the companies that gave DB transfer advice; and

- Concerns over the state of the UK economy both from a Covid-19 recessionary basis and from the uncertainty surrounding our exit from the EU.

Market pressures

Like any marketplace, price is a consequence of supply and demand. The supply side has been constrained since the Lloyd’s of London review of May 2018, following a significant underwriting loss in the 2017 year of account.

The Lloyd’s franchise board acted to look at poorly performing syndicates and more scrutiny was placed on poorly performing lines of business – non US PI being one of those lines of business being identified.

This meant a number of syndicates came under scrutiny – some had to represent their business plans and for some this meant they had their capacity reduced, some pulled out of the class and indeed some ceased underwriting.

This had an effect on a number of classes of business and PI insurance in particular.

With increasing premiums came a further squeeze on capacity, as the insurers’ capacity is used at a faster rate, meaning they are unable to insure as many risks.

The shrinking of capacity and pressure on premium pricing is referred to as a hard market and typically we get to a stage where the premium pricing attracts new entrants to the market in order to take advantage of this opportunity.

This usually creates competition and then we start to see premiums fall again, leading to what is known as a soft market.

At present, a number of potential new entrants to providing insurance solutions to the profession are concerned about the volatility of this class of business.

Long-term practitioners will not need reminding of previous issues with the original pension review: Splits and Scarps, Arch Cru, Keydata, Harlequin, pension ETVs and UCIS.

Insurers cite and draw comparisons between what we are facing today and the difficult years following the global financial crisis, and the claims that emanated from this, significantly increasing volumes and values through 2010, 2011 and 2012.

The class has generally been quite profitable for insurers since then.

As an insurance broker, and specialists on behalf of the profession, we take our role very seriously in trying to persuade insurers to remain in the market and also look to provide statistics and commentary to either persuade new insurers or previous insurers to re-enter the market.

We strongly believe that insurers’ concerns around the profession are, in some instances, overstated. For the considerable majority, there is a keen sense of doing the right thing for their clients in a suitably compliant fashion.

So what can you do to help?

- Proposal forms are long and complex – but please pay attention to the detail and add supplementary information. You are using this to sell yourself to the insurance underwriter. While people continue to work remotely and with huge workloads, a badly completed form, or one that is difficult to read, will potentially go to the bottom of the pile.

- If you have been advising on DB pension transfers, supply as much information as possible to support the resilience of your processes. As we have seen from the various FCA reviews, the number of cases on which you advised and the ratio of numbers transferred from the whole population are important. We all know that a number of companies and their advisers turned away many potential transferees who clearly would have been unsuitable for a transfer – anything about these volumes is useful. As of course are those that transferred and remain with you as active clients receiving ongoing advice.

- Discuss the timing of your submission with your broker. Get information together in plenty of time (at least six weeks in advance) and leave time in case there are additional questions.

All insurers, whatever the profession of their client, are interested in how your business has been impacted by the pandemic. Include a few paragraphs around how you have been working, how compliance and regulatory responsibilities have been catered for, how your income has been impacted and your expectations for the future.

This is all valuable information that can assist your broker.

This article was originally posted on FTAdviser.com and can be found here.

Chris Davies

Chris' team of expert brokers specialises in Professional Indemnity for Financial Advisers, Accountants, and Insurance Brokers. They always work hard to get their clients the right cover for the right price. And Chris' deep understanding of risk management means that he can help clients mitigate their risks as well as insuring against them.