The insurance market look out

Published

Read time

The ever-changing insurance market and the future of terms and pricing for Wealth Managers and IFAs.

Wealth Management and Financial Advisory, although closely linked and in some firms co-located under one roof, are often dealt with by two entirely different sets of insurance underwriters. Typically, Financial Institutions underwriters work with Wealth Managers and Professional Indemnity Insurance underwriters work with IFAs. This involves two separate profit centres, different experiences and different concerns.

This has meant that insurance brokers have also grown up with two separate teams. Howden is different in that it has experts from both fields working in unison and in this article experts from the Howden team provide a commentary on the current insurance market for Wealth Managers and IFAs and what they expect to happen in the near future.

Wealth Managers

The Financial Institution (FI) insurance market has followed the trend of the insurance market at large; between 2010- 2018 the supply of capital and underwriting appetite was reasonably abundant and brokers were therefore able to negotiate improved pricing and broader cover at almost every renewal – so long as the Wealth Manager’s risk profile hadn’t materially altered (claims, acquisitions etc).

By the summer of 2018 insurers’ margins had evaporated, the inevitable result of eight years of increasing cover and diminishing rates, coupled with increasing claim frequency and severity. In 2019, Lloyd’s of London was forced to review all of its syndicates’ strategies and so began the start of a hardening market. More recently, the Covid-19 pandemic has inevitably caused further disruption.

Now the current economic downturn and continued uncertainty creates further potential liabilities for financial institutions from an insurance perspective. Our market data has average premium hikes for a like-for-like renewal currently between 10% and 20% for a Wealth Manager depending on the size of the limit purchased; and it’s important to work closely with your Broker to ensure you are at the lower end. Other FI sectors such as Private Equity are well in excess of that.

Looking to the future

This market correction is predicted by Paul Towler, Howden’s Chief Broking Officer, to be the most significant since the 1986-1987 ‘Lloyd’s crash’ and further premium increases are likely at next renewal, on top of those incurred at this renewal. Quite how long the hard market endures will depend largely upon the inflow of ‘new’ underwriting capacity. The good news is that this can happen quite swiftly, as it did post the financial crash hard market in 2008-2009, but quite when capital providers will deem the moment right this time round remains to be seen.

According to Howden, it is now crucial to mitigate the increases;

- Your insurer relationships should be properly leveraged - hopefully your broker has spent time doing this for you, finding ways to put your business first on an insurer’s renewal list

- Ensure your specific risk differentiators are properly understood, articulated and factored into the pricing by underwriters. Your broker should guide you

- You are given time to provide the right information to insurers. There is no excuse for being last minute, especially in the current climate

- Be inquisitive and challenge your broker. Make sure they understand your sector, have the experience to deliver and are speaking to all of the market

- Consider the limits you buy, your renewal dates and your insurance structure. Is this the right fit for your business and how has this been tested? Do you have confidence your coverage is fit for purpose in the event of a claim?

Remember that whilst pricing is a factor, be careful, the robustness of your cover is vital. Your broker should have an answer for that too! Ask them.

IFAs

The IFA world is not dissimilar to the message above, but certainly the financial press is full of more tales of woe for Financial Advisers: increasing FCA fees, increasing FSCS levies, reducing income and massively increased Professional Indemnity Insurance (PII) costs. Whilst we have a view on all of the above, the PII market and the actual costs of policies is the focal point for this article.

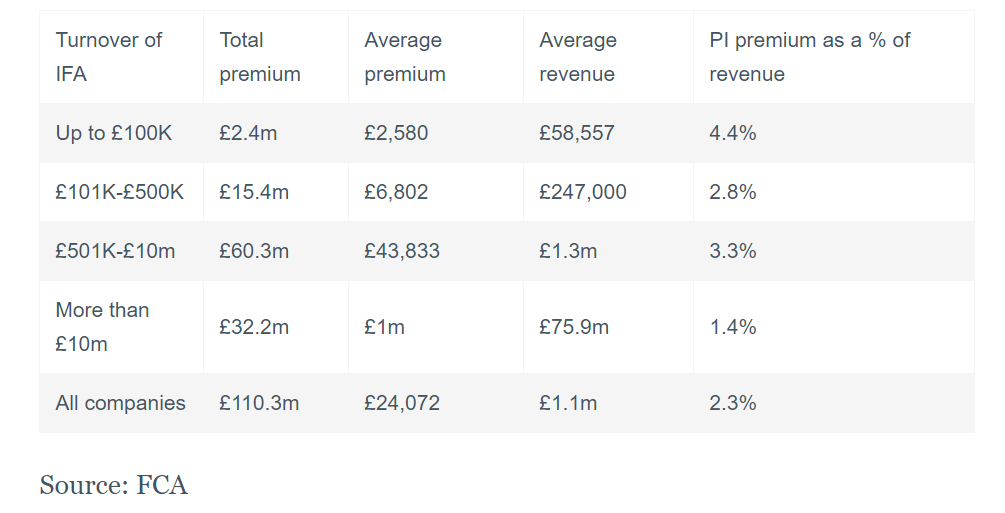

Any firm which has had a recent renewal will know that premiums have increased, in fact they have done consistently for two years now, but a look at the table below compiled from the FCA’s own figures) will put the premium rates into context.

Our figures tend to be a little lower per band. It is of course very difficult to generalise, so a firm which has undertaken a significant number of Defined Benefit Transfers (DBTs) will likely pay a very different premium to one that doesn’t, as will a firm which has had a number of claims in the past compared to one that is claim free.

However, to build on John’s macro points above regarding the insurance market itself, the state of the UK economy both from a Covid-19 recessionary basis and from a bad Brexit, what else is driving these IFA figures, bearing in mind average rates for IFAs were between 1% and 1.5% (depending on business mix) for a number of years?

- We have found that there is a lack of insurance capacity for IFAs. With only five or six insurance markets and a general lack of interest in new business the ability to source competitive alternative quotes is extremely limited

- Insurers’ concern over the now maximum FOS award of £355,000

- The FCAs continuing investigation of the firms that gave DBT advice

What are we doing to help IFAs?

As an insurance broker, and specialists on behalf of the profession, Howden are working hard to find new insurers to enter this market place and clearly it will only be at this stage that some sense of normality will return. We strongly believe that insurers’ concerns around this profession are unfounded with, for the considerable majority, a keen sense of doing the right thing for their clients in a suitably compliant fashion.

We are advising our clients to:

- Pay attention to the detail and add supplementary information to their proposal forms. You are using this to sell yourself to the insurance underwriter. While people are working remotely and with huge workloads, a badly completed form or one that is difficult to read, may go to the bottom of the pile.

- Discuss the timing of your submission with your broker. Get information together in plenty of time and leave time in case there are additional questions.

- All insurers, whatever the profession of their client, are interested in how your business has been impacted by the pandemic. So, include a few paragraphs around how you have been working, how compliance and regulatory responsibilities has been catered for and what has happened to your income.

Article written by:

John Greene, Divisional Director, Howden.

Lindsay Ratcliffe, Divisional Director, Howden.

Steve Ray, Divisional Director, Howden.

This article was originally published in PIMFA's Journal, Autumn 2020.