Members

Combined cover for when you need it most

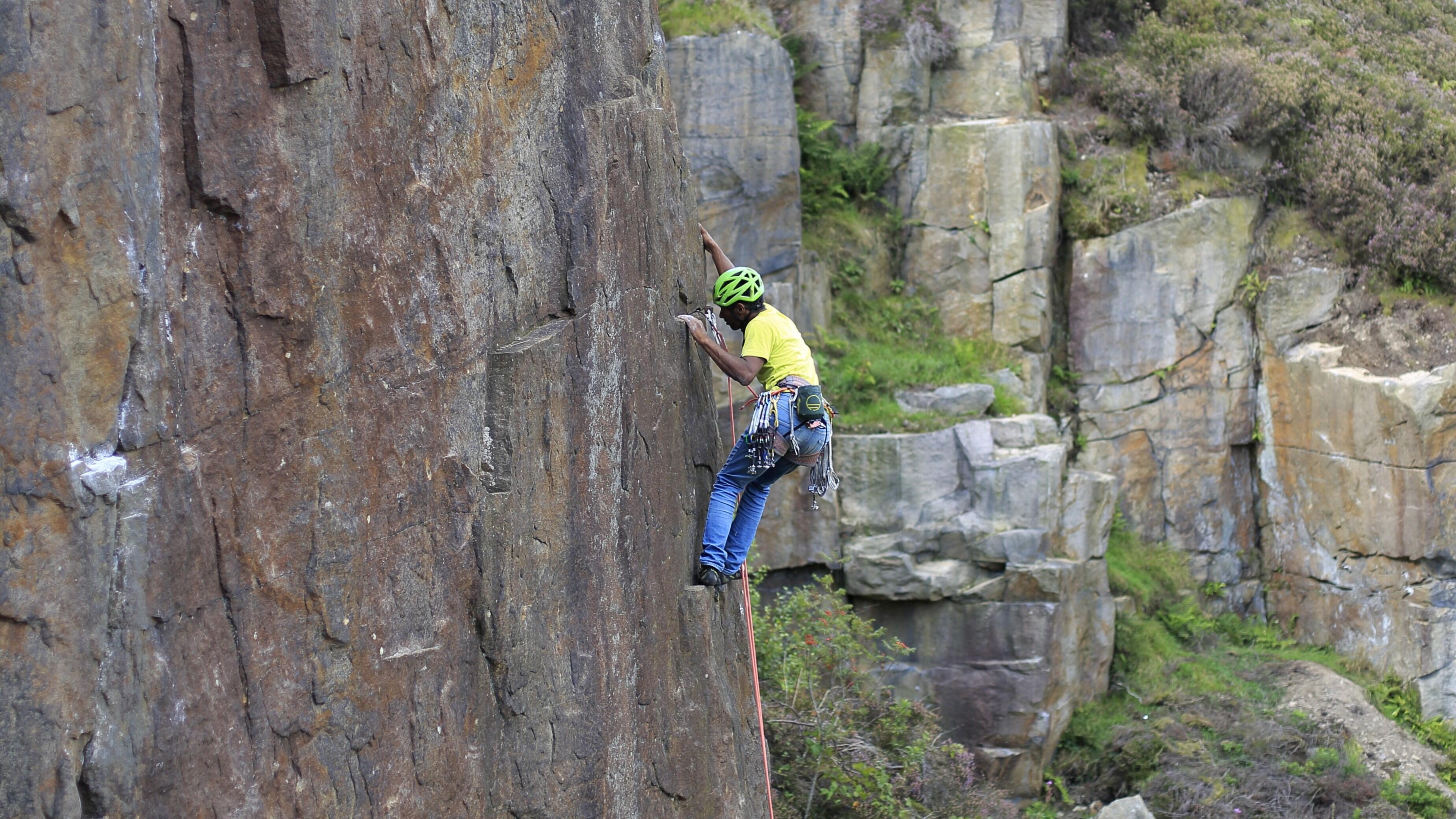

As a member, you are provided with Combined Liability and Personal Accident protection for your mountaineering activities.

Incidents happen. That's why all sports organisations have full and appropriate insurance protection. Without it, individuals can be held personally financially liable to compensate for losses for which you do not hold valid insurance.

Combined Liability cover

Combined Liability provides protection from the consequences of claims against a BMC member for injury, financial loss or damage to property, where negligence occurs.

Accidents in mountaineering can and will happen and members can be vulnerable to claims involving very large sums of money. Combined Liability provides a breadth of cover that is rarely available through non-specialist brokers, providing cover for legal liability under civil law to the general public for personal injury or damage to third party property.

All members of BMC have a responsibility to ensure that anything they do does not cause injury or financial loss to others or damage to property. If they do, and negligence is proved, they could become legally liable to pay compensation.

Advising other members

Being part of a club gives you the opportunity to give support and guidance to less experienced members. As part of your cover, you will be insured for giving free, unpaid advice to other members of your club on a voluntary basis.

Personal Accident cover for individual members

Personal Accident cover provides “no-fault” compensation to individual members if you suffer a permanent disabling injury whilst participating in mountaineering activities.

For terms and conditions go the the policy hub page to download your policy documents.

Here are some frequently asked questions about cover for members

Combined Liability Insurance provides for legal liability following negligence, nuisance or trespass. Unlike other liability insurances, it not only covers Public Liability (where you are liable for injury or damage to other persons or their property), but also includes cover for the following, which are excluded from other providers standard covers:

- Professional Indemnity – injury following advice or instruction given by an individual or club member operating in voluntary capacity

- Directors and Officers cover – for decisions made by club committees

- Libel & Slander – liability following something you might have said or written down (including website, emails etc.)

- Abuse – liability incurred by a club as a failure of their duty of care

Cover includes recognised activities, which include:

- Climbing indoor and outdoor

- Winter and summer mountaineering

- Rock climbing

- Abseiling

- Scrambling

- Gorge-walking

- Canyoning

- Hill walking

- Low-level walking

- Guided walks

- Fell and mountain running

- Slack lining (not high lining)

- Navigation

- Camping

- Tyrolean traverse

- Bouldering

- Coasteering

- Route setting

- Emergency first aid in the outdoor

- Ski-mountaineering

- Orienteering

- Ski touring

Secondary activities including mountain biking, canoeing/kayaking or caving, but only when carried out as part of a club meet and undertaken by those members who are competent in the particular activity (ie not novices).

Representation on any management committee or acting as a trustee with respect to the operation of mountaineering huts

Combined Liability is designed specifically to meet the needs of the organisation and its affiliated individual members, club members and Associations.

This includes the following:

- Individual Members and Club Members

- Club Volunteers

- Hut Wardens

- Trustees of clubs

- Employees

- Committee Members

- Officers, Trustees and Volunteers

There is no age limit in respect of Combined Liability cover. Personal accident cover is available to members up to the age of 80.

Insurance cover is only available to fully paid up members who have a permanent UK address. Such members are covered for mountaineering activities in both the UK and overseas (but excluding USA and Canada). Members with a permanent UK address who are working on a temporary contract or serving with the armed forces abroad are included within the cover, for mountaineering activities in both the UK and overseas (but excluding USA and Canada).

Any member permanently living abroad is not covered because the policy is subject to UK jurisdiction and the underwriters will not extend cover to permanent overseas residents.

Combined Liability will provide protection for your potential legal Liabilities, however; if you are going abroad you should take out specialist travel cover. You can arrange this through the BMC on their website.

Exclusions or limitations include:

- Risks that require more specific insurance, i.e. Motor, marine

- Loss of or damage to property in your custody or control

- Pollution unless caused by a sudden identifiable unintended and unexpected incident

- Any legal action brought against the insured in a court of law within the United States of America or Canada other than where a member is in USA or Canada

- Fines, penalties or punitive damages

- Damage to products supplied and work and the repair, replacement or recall of same work

- Claims arising out of or in connection with asbestos

- Repair of defects in premises disposed of

- Claims arising out of or in connection with damage to any data

- Nuclear risks

- War risks

- Deliberate, dishonest or foreseeable acts

- Infringement of trademark name registered design copyright or patent right

- Medical negligence

- Abuse - the person accused of abuse / alleged to be the abuser. Charges of abuse against an individual are brought under criminal law and as such are not covered by this policy.

- Claims arising from loss happening prior to the retroactive date stated in the schedule, which would be the date that your continuous membership first commenced.

- Incidents / claims known to you but not reported to the insurers immediately

In the event of a claim your limit of indemnity is the maximum your policy will pay. Howden recently handled a catastrophic injury claim which paid in excess of £10m. As claims inflation costs increase, the need for a higher limit of indemnity to protect you is vital.

There have been cases of members of sports clubs having disputes within clubs. Posts on websites and contained in emails could also be potentially libellous, for example.

Yes, but only for:

- Legal expenses for defence of actions.

- Legal Defence Costs are included for the defence of criminal actions brought in respect of a breach of the Health & Safety at Work Act 1974 and Section II of the Consumer Protection Act 1987. The Limit of Indemnity if £250,000.

If you are charging for your services as an instructor, no. You are only covered if you are instructing on a voluntary basis and are not being remunerated for your work.

You should immediately record relevant information concerning incidents involving a fatal accident, an injury involving either referral to or actual hospital treatment, any allegations of libel / slander, any allegations of professional negligence, i.e. arising out of advice given, any investigation under any child protection legislation or any circumstance involving damage to third party property. You must report every claim and any incident that is likely to give rise to a claim in the future.

Incident Notification Guidelines are included elsewhere on the site. Do not admit liability; do not make an offer or promise to pay. Please see separate instructions and Incident Report Forms on this site.

We're always here to help

For an queries regarding insurance, speak to a helpful representative at Howden