Iran conflict escalation: systemic risk implications for Australian organisations

Iran conflict escalation: systemic risk implications for Australian organisations

The escalation of conflict involving Iran is rapidly evolving beyond a regional security issue into a systemic global disruption with direct and cascading consequences for Australian organisations. The concentration of instability around critical energy and trade corridors, particularly the Strait of Hormuz, is now impacting oil and gas markets, global shipping routes, aviation pathways, and insurance availability.

For Australia, the implications extend well beyond fuel prices. The current environment is characterised by converging risks across energy, supply chains, cyber security, insurance markets, and access to critical raw materials. These dynamics are not isolated or short-term; they represent the early stages of a prolonged disruption that may reshape operational resilience requirements across multiple sectors.

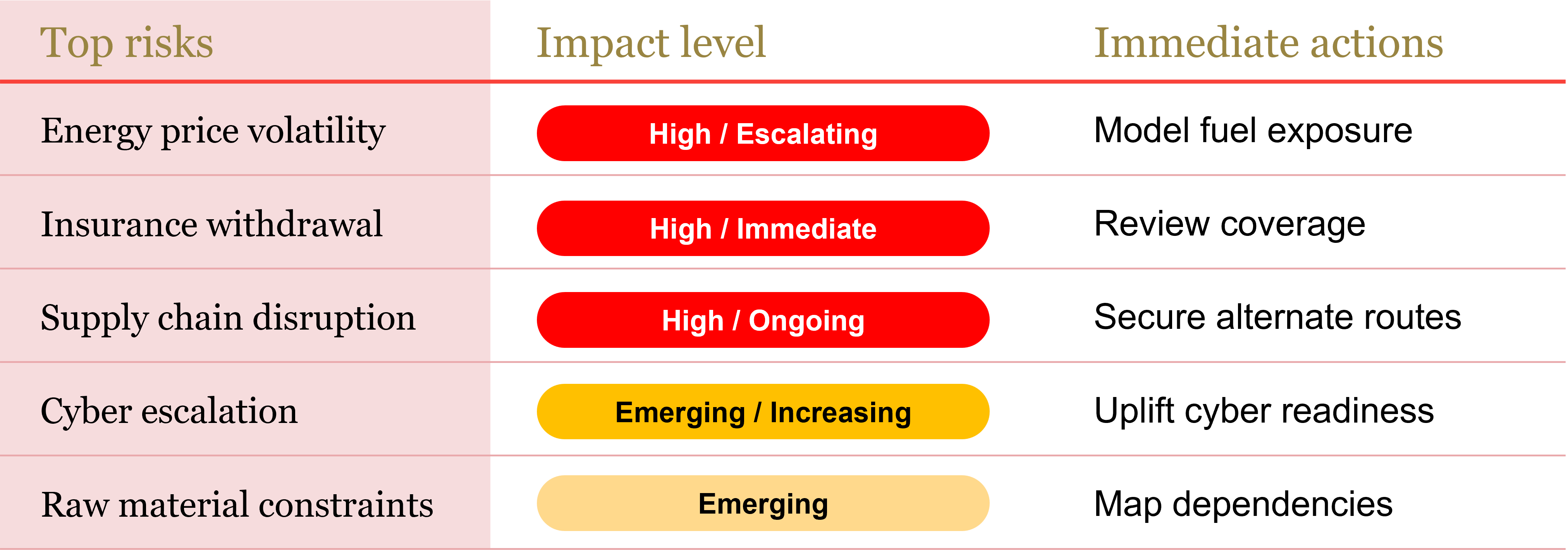

Risk dashboard

The nature of the disruption

The Strait of Hormuz remains one of the world’s most critical chokepoints, facilitating a significant proportion of global oil and liquefied natural gas flows. Escalation in the region has already resulted in shipping delays, rerouting, and in some cases the withdrawal or repricing of war-risk insurance, which is fundamentally altering the viability of trade through the region.

Energy markets are reacting first, with increased volatility in oil and gas prices. However, the more significant risk lies in the cascading effects. As insurers withdraw cover, shipping operators and logistics providers are forced to suspend or reroute operations, creating systemic disruption rather than incremental delay. Iran is increasingly targeting regional energy infrastructure, including oil and gas facilities. Should missile or drone strikes cause significant damage to upstream production assets, refining capacity, or export pipelines, the resulting outages could create longer-term supply constraints across global energy markets.

At the same time, the conflict environment is driving an increase in state-aligned cyber activity targeting critical infrastructure, logistics platforms, and energy systems. This extends the disruption beyond physical supply chains into the digital systems that underpin them.

Additionally, the Middle East’s role as a key producer of petrochemicals, fertilisers, and industrial feedstocks is introducing emerging pressure on global raw material supply chains, with lagging but potentially severe impacts to manufacturing, agriculture, and pharmaceuticals.

Sector-level impacts and emerging risk exposure

In the energy and utilities sector, organisations are experiencing immediate cost pressures driven by fuel price volatility and supply uncertainty. However, the more structural risk is the potential for intermittent supply disruption combined with pricing instability, particularly if shipping constraints persist or damage to production assets occurs.

The transport and logistics sector is facing a dual disruption. Physical constraints through key shipping routes are being compounded by insurance withdrawal, which in some cases is preventing vessels from operating altogether. This is transforming disruption from delay into complete unavailability of routes, with cascading impacts across global supply chains.

In agriculture, the exposure is expanding beyond fuel costs. Disruption to fertiliser and chemical inputs, many of which are derived from Middle Eastern production, creates a secondary supply risk that may impact crop yields, input costs, and long-term productivity.

Manufacturing and industrial sectors face a similar challenge. Reduced availability or increased cost of petrochemicals and industrial feedstocks can disrupt production cycles, delay outputs, and increase reliance on alternative suppliers, often at higher cost or lower reliability.

The aviation and tourism sector is experiencing immediate operational disruption due to airspace restrictions and safety concerns. However, this is being compounded by rising fuel costs and insurance constraints, which may reduce viability of routes over time and reshape travel patterns.

Across financial markets, the convergence of energy volatility, supply chain disruption, and geopolitical uncertainty is reintroducing inflationary pressure and market instability. Organisations are increasingly exposed to cost unpredictability and shifting economic conditions, which may impact investment decisions and long-term planning.

Escalation pathways and forward risk outlook

If the conflict persists or escalates, disruption is likely to deepen and broaden across both physical and digital domains. Sustained pressure on energy flows may entrench higher fuel costs, while ongoing insurance withdrawal could continue to constrain global shipping capacity.

Cyber warfare is likely to intensify, particularly targeting critical infrastructure and globally connected systems. This creates a scenario where organisations may experience disruption, not only through supply chain impacts, but through direct interference with operational technology and digital platforms.

At the same time, disruption to raw material supply chains may begin to manifest more visibly, creating shortages or cost spikes in sectors that are not traditionally associated with geopolitical risk, such as agriculture, pharmaceuticals, and advanced manufacturing.

These risks are interconnected. A disruption in one domain, such as insurance or cyber, can rapidly propagate across energy, logistics, and production systems, amplifying overall impact.

Strategic considerations for Australian organisations

The current environment requires a shift from isolated risk management to integrated, system-level thinking. Organisations must recognise that exposure is often indirect and may arise through suppliers, service providers, or digital dependencies rather than direct regional presence.

For example, a construction firm may initially experience rising fuel costs, but over time may also face delays in material imports, increased insurance costs for projects, and potential disruption to subcontractor availability. Similarly, an agribusiness may face fertiliser shortages not as an immediate shock, but as a delayed consequence of upstream disruption in petrochemical supply.

Cyber risk must also be reframed in this context. The convergence of geopolitical conflict and digital infrastructure means that cyber incidents should be anticipated as part of the broader disruption landscape, rather than as isolated events.

Organisations that are able to map these interdependencies and understand how disruption may cascade across systems will be better positioned to respond effectively.

Priority actions aligned to emerging risk drivers

Energy and cost exposure management

Energy shock

Identify exposure → Model sustained scenarios → Adjust financials → Lock pricing / renegotiate → Protect margins

Organisations should immediately assess their exposure to sustained fuel and energy price volatility across operations, logistics, and supplier networks. This includes modelling scenarios where elevated fuel costs persist for several months, rather than short-term spikes, and understanding how these costs flow through transport, procurement, and service delivery.

Financial planning should be adjusted to reflect increased uncertainty in freight and input costs, with reforecasting of cashflow under disruption scenarios. Where possible, organisations should consider locking in pricing or renegotiating supplier agreements to reduce margin compression, while maintaining flexibility to respond to further volatility.

This is not solely a cost issue but a strategic exposure. Energy price instability has the potential to erode margins, delay projects, and impact competitiveness if not actively managed.

Supply chain and raw material security

Supply disruption

Map dependencies (Tier 1 - 3) → Identify route & supplier risks → Activate alternatives → Secure critical inputs → Maintain continuity

Organisations need to move beyond Tier 1 supplier visibility and map exposure across extended supply chains, including logistics providers, transport corridors, and upstream dependencies. Particular attention should be given to routes transiting the Middle East, as well as secondary congestion risks emerging in alternative global corridors.

Alternative sourcing and routing strategies should be identified and, where possible, pre-approved to enable rapid activation. This includes shifting between air and sea freight, utilising different regional hubs, and increasing inventory buffers for critical goods.

A key gap in many organisations is visibility over raw material dependencies. Inputs such as petrochemicals, fertilisers, and industrial feedstocks, many of which are linked to Middle Eastern production, should be identified and monitored. Early engagement with suppliers is critical to understand availability risks, lead times, and contingency options.

The objective is to shift from reactive supply chain management to proactive control over availability, continuity, and substitution options.

Insurance, contracts and market access

Insurance withdrawal

Validate coverage gaps → Assess contract exposure → Engage suppliers/customers → Plan for shutdown scenarios → Maintain operability

Insurance withdrawal is already emerging as a critical constraint, with war-risk cover being reduced or removed in affected regions. Organisations should urgently review their exposure to insurance limitations across shipping, aviation, project delivery, and asset protection.

This includes validating whether existing policies remain applicable under current conditions, identifying exclusions related to conflict zones, and assessing the financial and operational implications if cover is withdrawn.

Contractual exposure must also be reviewed. Force majeure clauses, delivery obligations, and penalty provisions should be assessed to understand how disruption may impact contractual performance. Organisations should engage proactively with suppliers and customers to clarify expectations and reduce the likelihood of disputes.

Importantly, planning assumptions should shift from delay-based disruption to scenarios where operations may cease entirely due to lack of insurance or legal viability.

This represents a fundamental change in risk profile and requires executive-level visibility.

Cyber and operational resilience

Cyber escalation

Identify critical systems → Strengthen controls & segmentation → Test response capability → Monitor threats → Maintain operations under disruption

The escalation of geopolitical conflict is likely to drive increased cyber activity targeting critical infrastructure, logistics platforms, and operational systems. This risk is heightened by Iran’s long-standing use of state-sponsored cyber operations as an asymmetric tool against Western interests, including campaigns targeting critical infrastructure and essential services. Organisations should treat cyber risk as a parallel disruption pathway rather than a standalone IT issue.

Critical systems supporting logistics, supply chain visibility, and operational technology should be reviewed for resilience, including access controls, system segmentation, and backup capabilities. Incident response plans should be validated against scenarios involving concurrent cyber and physical disruption.

Monitoring of external threat intelligence should be increased, particularly for sectors linked to transport, energy, and infrastructure. Organisations should also recognise that cyber incidents may present as operational failures, such as system outages or data disruption, rather than clearly identifiable attacks.

Maintaining operational continuity in this environment requires the ability to detect, respond to, and recover from cyber disruption while other systems are under pressure.

Workforce, travel and continuity

Travel disruption

Identify critical roles → Shift to alternative delivery models → Update travel controls → Track workforce → Sustain operations

Organisations should identify critical roles that rely on international travel, including executives, technical specialists, and offshore project staff, and assess whether these functions can be supported through alternative arrangements.

Travel policies should be updated to reflect current conditions, including pre-approved alternative routing options and clear criteria for essential versus non-essential travel. Increased use of virtual engagement should be embedded to reduce reliance on physical movement where possible.

Duty-of-care obligations must be reinforced through real-time tracking of personnel in affected or transit regions, with clear escalation and communication protocols. Travel insurance coverage should be reviewed to ensure it remains valid under evolving conditions.

At an operational level, organisations should validate business continuity arrangements, including remote working capability and crisis management processes. Planning should incorporate scenarios where disruption is sudden and sustained, rather than gradual, ensuring the organisation can continue to operate under constrained mobility and reduced access to global networks.

Summary

The Iran conflict represents a shift from regional instability to systemic global disruption, with impacts already visible across energy, logistics, insurance, cyber security, and raw material supply chains.

For Australian organisations, the risk is not limited to the immediate disruption itself, but to how shocks propagate through tightly interconnected systems over time, amplifying operational, supply-chain and market impacts.

Organisations that proactively address these converging risks, particularly cyber warfare, insurance withdrawal, and raw material dependency, will be better positioned to maintain continuity and resilience in an increasingly volatile environment.

This article was prepared by our Risk Advisory team and our strategic risk partner Sention