Letter writing for claims – hints and tips

Published

Read time

An integral role in dealing with claims against your firm is responding to correspondence that you have received. Whilst Insurers are there to assist and guide you, under the terms of your policy you are required to provide full co-operation and assistance with the investigation, defence, settlement, or mitigation of any actual or potential claim. Insurers will therefore often request that letters are drafted by you. Whilst this can be time consuming, it helps you to retain control over correspondence and the relationship with your client as sometimes Insurers’ drafting may not be the most appropriate as you know the situation best.

To assist you in getting this right first time, we have pulled together some hints, tips and advice based on our experience of reviewing and discussing draft responses with Insurers to try and hit the nail on the head with the first draft.

Hints & tips

DO

- Give yourself enough time to draft a suitable response and also try to allow time for Insurers to consider this.

- As far as possible, respond in a timely fashion to avoid the matter escalating and the possibility of criticism from your regulators.

- Stick to the facts as much as possible. It is best to avoid using emotive language and try to refrain from sending overly detailed responses unless it is essential, as this can encourage unnecessarily lengthy correspondence that goes beyond the issue in hand.

- When acknowledging the complaint, set out the timescales contained within your complaints procedure. This will save you being chased by your client and helps manage their expectations. If it becomes clear you cannot make the indicated timeframes, inform the client accordingly.

DON'T

- Do not make admissions or inferences of acceptance of liability unless previously discussed with your Insurers.

- Do not make any offers to settle or indemnify any losses within your letter unless this has been discussed and approved by Insurers.

- Make sure that you do not send any correspondence without reference to your Insurers. This can open a door for Insurers to take issue with this and in serious cases, reserve their rights under the policy. If you have a tight time frame, please give us a call or mark your email as urgent and we will do all we can to respond quickly and obtain urgent instructions where required.

- Do not over complicate matters. As above, stick to the facts to avoid a client’s ability to draw inferences from comments or omissions that were not necessarily required in the response.

- Do not try and rectify the mistake or make offers to do so without the prior consent of your Insurers. It will not always be appropriate.

Pressure to put it right

If you consider that your firm’s conduct was negligent, care must be taken when attempting to put things right for a client. You may be aware of the case of Howell Jones. In this matter, Howell Jones acted for a husband in divorce proceedings and they did not receive a favourable outcome for him. Howell Jones gave their client the option to put matters right at their own expense (by attempting to have the decision overturned) and advised their client of a cause of action against them and to seek independent advice. The SDT concluded Howell Jones had “not ceased acting when it should have done and this was fairly described as an error of judgment”. Howell Jones were penalised for this cause of action and the overall cost to the firm and/or Insurers totalled around £150,000.

There is, of course, a requirement to be open and honest with clients if things go wrong (as per the recent changes to the Code of Conduct). This can include making factual admissions; however, it is best to run this past Insurers first. If you consider there to be a conflict of interest, it will likely be preferable for you to cease acting and advise the client to seek independent legal advice, even if this might not appear to be the most commercially savvy decision to your practice.

Importance of obtaining advice from insurers

You will of course be aware that there are certain obligations under your Professional Indemnity policy to keep Insurers in the loop and not to undertake any steps which may prejudice Insurers’ position. It is therefore important to ensure that Insurers are taken along for the ride and ‘buy in’ to any strategy that you wish to adopt. Remember, Insurers don’t like surprises!

The risks of not obtaining prior authority from Insurers can be serious. Insurers can reserve their rights under the policy if they would not have agreed to a particular course of action that has been undertaken without their consent. For example, if a letter has already been sent admitting liability but Insurers think the claim could have been defended, they may feel as though their position has been prejudiced. Similarly, Insurers will not be happy if an offer has been made above the policy excess without their consent as they may be committed to settling the claim and paying out before they have had a chance to comment.

What this reservation of rights means for you is that Insurers could seek a reimbursement from you to the extent they feel they have been prejudiced. It is therefore imperative that draft letters are sent to Insurers for their prior approval. Most importantly, it protects your position as Insurers are precluded from later saying that they would have dealt with matters differently, particularly if the position deteriorates.

Now that we have set out some hints and tips and explained the importance of drafting letters, below we have included some practical examples of phrasing things in an Insurer friendly way.

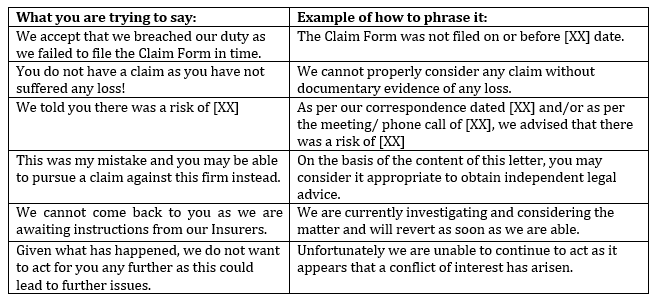

Wise words and phrases

Conclusion

Always remember that Howden and Insurers are there to assist you in reaching the best possible outcome of any claim/potential claim notified under the policy. Both we and Insurers see these claims on a daily basis so our knowledge and advice is always available - make sure you benefit from this knowledge. It may be, for example, that we/Insurers have successfully defended a similar matter in the past and have a number of helpful arguments that can be suggested to you to incorporate into your draft letter. Or perhaps you know what you want to say but are struggling to particularise this in a letter. It is always helpful to have another pair of eyes to provide extra guidance.

As we have touched on above, if timing is an issue, please let us know. It can be easy to be put off running a draft letter past Insurers if there is an urgency to respond. However, for the reasons mentioned in this article, we would caution against this. Instead, flag the urgency with us and we can expedite the matter with Insurers.

Please also bear in mind that some Insurers use third party claims handlers who may be able to prepare draft letters on your behalf. Please contact us find out more about your specific claims handling arrangements.

Ultimately, please remember that we are all on the same side so there is no downside in seeking guidance from us and/or Insurers. We would encourage you to make the most out of your policy and both we and Insurers fully appreciate that you may not be used to dealing with contentious matters on a regular basis, if at all.

Our specialist solicitors’ claims team at Howden are always happy to discuss matters with you and offer guidance in relation to draft letters or notifications generally. Please do not hesitate to contact your designated claims specialist.

Written by:

Nicola Vince, Howden UK

Senior Claims Executive

Professional Indemnity

Chloe Bingham, Kennedys

Associate